For years, Indian investors have faced a frustrating barrier — how to legally invest or send money abroad to pay overseas fees, or support family abroad without complicated approvals and restrictions. The Liberalised Remittance Scheme (LRS), introduced by the Reserve Bank of India (RBI), addresses this very challenge by allowing resident individuals, including minors, to remit funds abroad for permitted current and capital account transactions within a specified annual limit.

Restrictive Covenants

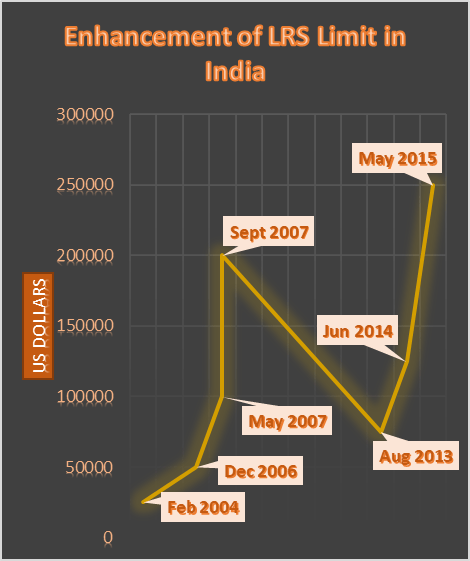

- Remittance Limit: As of the latest guidelines, an individual can remit up to USD 250,000 per financial year under LRS.

- Eligible Individuals: All resident individuals, including minors with a guardian, are eligible.

- Purpose of Remittance: Funds can be remitted abroad for various purposes, such as:

- Education

- Travel – private and business

- Medical treatment

- Gifts and donations

- Investment in shares, debt instruments, and property

- Maintenance of close relatives

- Opening and maintaining foreign currency accounts abroad

- Prohibited Transactions: LRS cannot be used for:

- Margin trading or speculative activities abroad

- Purchase of lottery tickets, banned magazines, sweepstakes, etc.

- Remittance for trading in foreign exchange abroad

Property Specifications

1. Eligibility:

The Liberalised Remittance Scheme (LRS) is available exclusively to resident individuals, including minors under the guardianship of an adult. Entities such as companies, partnership firms, Hindu Undivided Families (HUFs), and trusts are not eligible to participate in this scheme.

2. Permissible Transactions:

Under the LRS, individuals may remit up to USD 250,000 per financial year for the acquisition of immovable property abroad. This includes the purchase of real estate for residential or commercial purposes. The acquired property may be utilized for personal use, rental, or investment purposes.

3. Prohibited Transactions:

Remittances are prohibited for the purchase of property in countries designated as “non-cooperative” by the Financial Action Task Force (FATF) or in countries where the Government of India restricts remittance. Additionally, remittances for margin trading, speculative activities, or the purchase of lottery tickets are not permitted.

Procedures and Records

• Send the Authorized Dealer, bank a completed Form A2 together with a declaration outlining the reason for purchasing real estate overseas.

• Banks must conduct due diligence, confirm the funding source, and make sure the yearly capital is not exceeded.

• If the bank requests supporting documentation due to the nature of the transaction, provide it.

Adherence to Tax Law

• Tax Collected at Source (TCS): Applicable under current Income Tax Act regulations.

• TCS may be applied to specific remittances under LRS.

• The remitter must make sure the remittance conforms with Indian tax regulations and include the foreign asset in their tax returns as needed.

Contingencies

• The USD 250,000 capital is cumulative for all LRS-allowable transactions throughout a fiscal year, such as gifts, travel, education, share and real estate investments, etc.

• Specific RBI permission is required for remittances that exceed the limit or are used for ineligible purposes.

———————————————————————————————————————————————–

Source:

Purchase of Immovable Property

https://www.rbi.org.in/commonman/English/scripts/FAQs.aspx?Id=1855

Liberalised Remittance Scheme (Updated as on April 06, 2023)

https://www.rbi.org.in/Commonman/English/Scripts/FAQs.aspx?Id=1834